If you're still chasing checks, you're leaving money and clients on the table. The real question isn't "do attorneys accept credit cards?"—it's how much faster could you sign clients and improve cash flow if you made it simple for them to pay you on the spot.

This isn't about convenience anymore; it's a critical tool for winning new business.

Why Your Firm Can't Afford to Skip Credit Cards

In the race to sign new clients, friction is your biggest enemy. Every hoop you make a potential client jump through—like digging up a checkbook or finding a stamp—is a chance for them to hesitate. That hesitation is an open door for them to call the next firm on their list.

Accepting credit cards tears down that barrier, turning your firm's client conversion process from a multi-day waiting game into a decisive, single action. This isn't just about getting paid; it's about getting paid first. The data is clear: leads contacted within 5 minutes are 21x more likely to convert. Instant payment is a key part of that speed.

The numbers don't lie. Law firms that accept online credit card payments see a staggering 33% increase in revenue. They also get paid four times faster than firms waiting on checks. Offering a payment method everyone uses daily isn't just easier for clients; it fundamentally improves your firm’s financial health. You can discover more insights on how payments impact law firm revenue.

The Immediate Impact of Accepting Credit Cards

Integrating card payments has an instant, measurable impact on your practice. You aren't just adding another way to pay; you're upgrading your entire client conversion engine.

The benefits are clear:

- Secure Retainers Instantly: Get paid the moment a client decides to hire you. This eliminates the risky waiting period where they might get cold feet or call another firm.

- Fix Your Cash Flow: Funds from card payments typically hit your account within 1-2 business days. This gives you predictable revenue you can actually count on to run your business.

- Boost Conversion Rates: By making it effortless to pay, you dramatically increase the odds that a qualified lead becomes a paying client. It's a key part of optimizing your client conversion process.

Ultimately, accepting credit cards tells clients your firm is modern, efficient, and respects their time. It’s a small operational shift that delivers a major competitive advantage.

How Attorneys Get Paid: Cards vs. Checks

Still on the fence? This quick comparison makes the choice clear. For a small firm where every client counts, the right payment method makes all the difference.

| Metric | Accepting Credit Cards | Relying on Checks |

|---|---|---|

| Speed to Payment | 1-2 business days | 5-10+ business days |

| Client Convenience | High (Instant, familiar) | Low (Requires manual effort) |

| Conversion Impact | Increases sign-ups | Creates friction, leads to drop-off |

| Cash Flow | Predictable, fast | Unpredictable, slow |

| Failure Rate | Low (Declines are instant) | High (Bounced checks, lost mail) |

The takeaway is simple: checks slow you down, create risk, and cost you clients. Credit cards accelerate every part of your intake and revenue cycle.

The Hidden Cost of Being a "Checks-Only" Law Firm

Being a “checks only” firm in today's world isn't just an inconvenience—it's a direct threat to your bottom line. It actively costs you clients.

Think about it: a potential client decides to hire you. They're ready to move forward. If your next step is asking them to mail a check, you've just created a dangerous 24 to 48-hour cooling-off period where urgency fades and doubt creeps in. They might just call the next firm on their list that makes it easy to pay and get started right now.

This friction is a self-imposed roadblock to growth. It quietly signals that your firm might be outdated, which directly harms your ability to convert the leads you worked so hard to get.

Why Payment Friction Kills Your Conversion Rate

Put yourself in your client’s shoes. They're facing a stressful situation and want the fastest, clearest path to a solution. The firm that responds first and makes it easiest to get started almost always wins.

Every extra step you add is another chance for a lead to drop off. Waiting for a check to clear is a critical failure point. It creates a perfect opportunity for a competitor to swoop in with a simple online payment link and secure the client before your check has even been postmarked.

A striking 40% of consumers say they would never hire a lawyer who doesn't accept credit or debit cards. That’s a massive pool of potential clients you’re cutting yourself off from.

This powerful client preference is driving a huge shift. Today, 53% of law firms handle electronic payments—a number that’s climbing fast. You can read the full research about client payment preferences to see how quickly this is becoming the new standard.

The Real-World Impact on Your Bottom Line

The cost of not accepting cards goes beyond losing a few clients. It directly hits your firm’s financial stability.

- Delayed Cash Flow: Checks mean waiting days, sometimes weeks, for funds to clear. This creates unpredictable revenue and turns financial planning into a guessing game.

- Increased Admin Work: You and your staff burn non-billable hours chasing payments, going to the bank, and dealing with bounced checks. That's time you could be using to serve clients.

- Lower Collection Rates: The more time that passes between sending an invoice and getting paid, the lower the likelihood you’ll ever see the full amount.

By clinging to an outdated payment model, you are choosing to work harder for less predictable revenue. The question isn't "do attorneys accept credit cards?"—it's "can my firm afford not to?"

Solving The Ethical Puzzle: IOLTA Compliance and Credit Cards

Let's cut to the chase and tackle the #1 reason attorneys get nervous about accepting credit cards: the fear of messing up their trust account. It’s a valid concern, but the solution is straightforward. With the right tools, IOLTA compliance is a solved problem.

The biggest mistake you can make is using a generic payment processor like Square or PayPal to accept a retainer that belongs in a trust account. These platforms were not built for legal ethics.

When you use them, they deduct processing fees directly from the client's deposit before it hits your account. That’s an instant commingling of your firm's expenses with client funds—a serious ethical misstep.

What Is An IOLTA-Compliant Processor?

An IOLTA-compliant payment processor is a service built specifically for lawyers. It understands the non-negotiable wall between your operating and trust accounts.

These legal-specific processors solve the core ethical challenges in two critical ways:

- Fee Protection: They ensure 100% of the client's payment is deposited into your IOLTA account. All transaction fees are separately debited from your firm’s operating account. Zero commingling.

- Chargeback Management: If a client disputes a charge, the processor only attempts to pull funds from your operating account. This is huge. It protects other clients' money held in trust from being improperly seized.

Why This Matters for Retainers

When you accept a retainer, that money isn't yours yet. It belongs to the client until you perform the work. Protecting those funds is your highest ethical duty. Using a generic processor for a trust deposit is a compliance nightmare waiting to happen. To learn more, see our guide on how a retainer works with a lawyer.

The core principle is simple: Client funds in trust must remain untouched by third-party fees. A generic processor violates this rule by design; an IOLTA-compliant processor upholds it automatically.

Understanding Processing Fees and Profitability

Firm owners get hung up on processing fees. They see that 1.5% to 3.5% charge and think of it as a loss. It’s time to reframe that. The fee isn't a cost; it's a strategic investment in higher collection rates and faster payments.

Ignoring this is like refusing to pay for a delivery truck because of the price of gas, all while your competitor is delivering their products instantly online. You're getting stuck on a minor expense while losing the entire sale.

How Lawyer Payment Processing Fees Pay for Themselves

The math is overwhelmingly in favor of accepting cards. Firms that accept cards collect 33% more revenue and get paid four times faster. That massive revenue lift easily absorbs the small processing fee, leaving your firm with a significant net gain. You can find a deeper dive into how surcharging rules and fee benefits stack up in this helpful resource.

Let’s run the numbers on a simple scenario.

Scenario: Your firm bills $20,000 in a month.

- Without Cards (86% collection rate): You actually collect $17,200.

- With Cards (91% collection rate, 3% fee): You collect $18,200, then pay $546 in fees. Your net take-home is $17,654.

- Net Gain: You end up with an extra $454 in your bank account, plus you got paid weeks faster.

This simple calculation shows how accepting cards more than pays for itself through improved collections alone. It doesn't even factor in the new clients you'll win by offering a frictionless way to pay their initial lawyer retainer fee.

Analyzing the ROI of Attorney Credit Card Fees

Let's model this out. We'll use a conservative 5% increase in collection rate against a 3% processing fee.

| Billing Scenario | Without Credit Cards (86% Collection) | With Credit Cards (91% Collection, 3% Fee) | Net Revenue Gain |

|---|---|---|---|

| $50,000 Billed | $43,000 Collected | $44,135 Net Collected | +$1,135 |

| $100,000 Billed | $86,000 Collected | $88,270 Net Collected | +$2,270 |

| $250,000 Billed | $215,000 Collected | $220,675 Net Collected | +$5,675 |

As you can see, the higher collection rate doesn't just cover the fees—it generates substantial additional revenue for your firm.

Passing Fees to Clients: The Surcharging Option

If absorbing the fee is still a concern, you might have another option: surcharging. This simply means adding the credit card processing fee to the client's invoice.

However, this isn't a free-for-all. Surcharging is governed by a patchwork of state laws and card brand rules.

- Allowed States: Most states permit surcharging, but often cap the fee (usually around 3%) and require clear disclosure.

- Prohibited States: A few states, like Connecticut and Massachusetts, prohibit it entirely.

Before you consider a surcharge, you must check your state's current laws and ethics opinions. Remember, absorbing the fee often creates a better client experience and is a small price to pay for securing more revenue, faster.

How Your Law Firm Can Accept Credit Card Payments The Right Way

You've seen the numbers. Now it's time to put it into practice. Setting up credit card payments is one of the biggest operational wins for your firm, and you can get it done in three straightforward steps.

The goal isn’t just to accept a card. It’s to build a seamless experience where a new client signs their retainer, fills out their intake forms, and pays their deposit in one fluid motion.

Step 1: Choose Your Payment Processor

Your first decision is picking the right processor. Your choice boils down to one simple question: do you need to accept funds directly into a trust account?

- Legal-Specific Processors (IOLTA-Compliant): Services like LawPay and Gravity Legal are built for lawyers. They automatically handle IOLTA compliance for retainers without you having to lift a finger.

- Flexible Processors (Operating Account Only): A processor like Stripe is a fantastic, modern choice if you only take payments for earned fees directly into your operating account. It has powerful tech but is not designed for direct trust account deposits.

Step 2: Connect Your Bank Accounts

Once you've picked a processor, the setup is simple. You’ll securely link your firm’s operating account. If you chose an IOLTA-compliant provider, you'll also connect your trust account. The processor handles all verification and directs funds to the right place.

Step 3: Integrate Payments Into Your Intake Workflow

This final step is the most important. Don't just email your clients a generic payment link. Instead, unify the entire process. A platform designed for modern law firms is a total game-changer here.

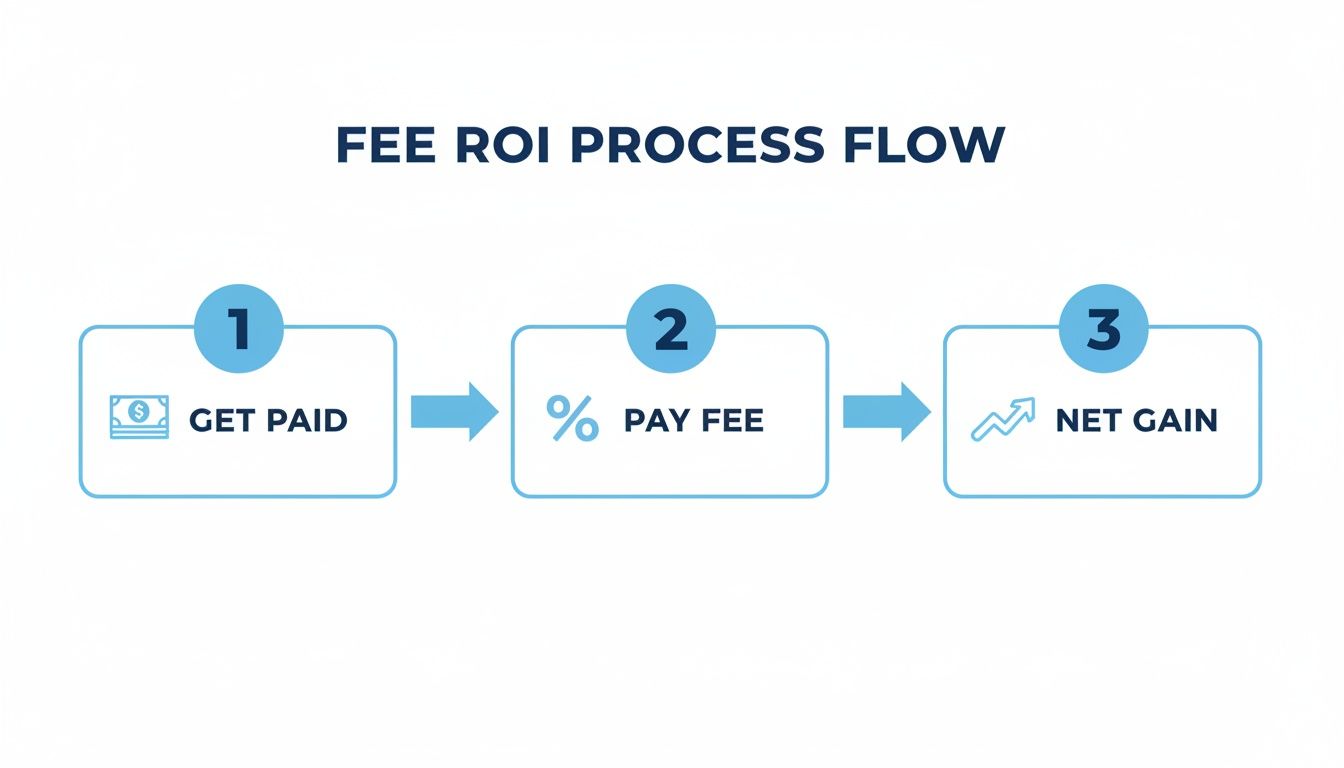

The infographic below shows the simple return on investment you get from this kind of efficiency.

This process visualizes how faster payments and higher collection rates easily cancel out the processing fees, leading to a clear net gain for your firm.

Instead of juggling separate tools, you can use a single platform to handle it all. By connecting your Stripe account to intake.link, you can generate one link where a client signs their retainer, completes forms, and submits payment—all in a single session. Top firms use client intake software for law firms to automate these crucial first steps. This unified approach closes the gaps where promising leads go cold.

Common Questions About Law Firm Payments

Ready to start? Here are straight answers to the questions we hear most from attorneys.

Can I Accept Credit Card Payments Directly Into My IOLTA Trust Account?

Yes, but only if you use an IOLTA-compliant payment processor. Don't even think about using a generic service like PayPal or Square for trust accounts. Legal-specific processors are built to pull fees from your operating account and manage chargebacks correctly, keeping you compliant.

What's The Difference Between a Legal-Specific Processor and a Generic One?

Think of it like this: a generic processor like Stripe or Square is an all-purpose tool. A legal-specific processor like LawPay is a precision instrument designed for one job: keeping you compliant. While you can use a generic processor for earned fees, a single legal-specific solution for everything is simpler and safer.

Should I Absorb The Fee or Pass It On To The Client?

This depends on your state's rules and your firm's preference. Many states permit "surcharging" (passing the fee on) if you disclose it clearly. But remember, the convenience of paying by card typically increases collection rates by 2-5%. Since fees are only 1.5-3.5%, most firms find it's profitable to just absorb the cost and provide a smoother client experience.

How Can I Make The Payment Process Seamless For New Clients?

Stop thinking about payment as a separate step. Integrate it directly into your client intake workflow. A modern intake platform lets a client sign their retainer, pay the deposit, and provide their info in one simple, branded flow. This dramatically reduces friction and helps you get retained before they have a chance to call another firm.

Stop losing leads to clunky, multi-step intake processes. intake.link combines e-signatures, intake forms, and payments into a single link so you can get retained before a client calls another firm. Stop losing leads—get signatures before they call another firm.