Losing a great client because they can't pay your entire retainer upfront is a huge, avoidable frustration. Offering flexible payment plans isn't just a courtesy; it’s a critical tool for boosting conversions and securing clients who might otherwise walk away.

The question isn't just "do attorneys take payment plans?" It’s "how do you use them to sign more clients without creating an administrative nightmare?" The answer is simpler than you think.

Why Payment Plans Are Your New Competitive Edge

In today's market, clients expect convenience. Refusing to offer payment options makes your firm seem rigid, sending qualified leads straight to competitors. Offering a payment plan immediately removes the single biggest hurdle for many potential clients—the upfront cost.

This isn't just a hunch. According to Clio's 2024 Legal Trends Report, a staggering 71% of clients prefer paying a flat fee, signaling a clear demand for predictable costs. The same report found that firms using modern billing models collect what they're owed nearly twice as fast. You can read more about these legal industry statistics and see how billing flexibility impacts firm growth.

By offering payment plans, you will:

- Increase Your Conversion Rate: You make your services accessible to a wider pool of qualified clients.

- Create Predictable Revenue: Monthly installments create a steady, reliable cash flow for your firm.

- Improve Client Satisfaction: Flexibility shows you understand your clients' financial realities, building trust from day one.

This is about turning a potential headache into your most powerful tool to stop losing leads and achieve faster conversions. With the right system, you can automate payments and focus on practicing law.

Traditional Billing vs. Modern Payment Plans

This table shows how the two models impact cash flow and client acquisition for small firms.

| Attribute | Traditional Hourly Billing | Automated Payment Plans |

|---|---|---|

| Cash Flow | Unpredictable; spikes and dips based on large one-time payments. | Consistent and predictable monthly revenue stream. |

| Client Acquisition | High upfront costs create a major barrier, losing many qualified leads. | Lowers the barrier to entry, significantly increasing conversion rates. |

| Client Satisfaction | Can create financial stress and friction at the start of the relationship. | Builds goodwill and trust by offering flexibility and understanding. |

| Administrative Work | Requires manual invoicing, collections, and chasing overdue payments. | Payments are automated, reducing staff workload and collection efforts. |

The contrast is clear. While traditional billing has its place, automated payment plans directly address modern client expectations and solve some of the most persistent administrative challenges small firms face.

Choosing the Right Payment Model for Your Practice

Not all payment plans are created equal. The key is to match the payment model to your specific practice area and the nature of the work.

Let’s break down three proven models you can put to work immediately.

Classic Installment Plans

This straightforward model works perfectly for flat-fee services like uncontested divorces, basic estate planning, or misdemeanor defense.

You simply take the total flat fee and slice it into a set number of automatic monthly payments. For example, a $3,000 flat fee could become an initial $1,000 deposit followed by four monthly payments of $500. This makes the cost manageable for your client and gives your firm predictable cash flow.

Evergreen Retainers

For ongoing litigation or complex cases where you bill hourly, the evergreen retainer is your best friend. Instead of chasing clients for replenishment, you automate the process.

Here’s how it works:

- The client pays an initial retainer, say $5,000.

- You bill your hourly work against that balance.

- When the balance dips below a set threshold (e.g., $1,500), the client's card on file is automatically charged to replenish the retainer back to $5,000.

This model eliminates accounts receivable for hourly work and ensures you always have funds to draw from. To dig into the mechanics, see our in-depth guide that explains how legal retainers work for lawyers.

Hybrid Models

Some cases don’t fit neatly into a flat-fee or hourly box. For multi-stage matters like a business formation with ongoing compliance work, a hybrid model offers the most flexibility.

This approach blends an upfront fee with predetermined milestone payments. You might charge an initial fee for discovery, then schedule additional fixed payments when you hit specific milestones, like filing a major motion. This gives clients clarity on what they're paying for at each stage.

How to Structure a Bulletproof Payment Agreement

A vague, handshake deal on payments is a recipe for chasing down invoices. Your retainer agreement must create total transparency from day one.

You need to set clear, professional expectations around payment schedules, automatic billing, and what happens if a payment fails. This clarity is the foundation of a healthy client relationship and ensures you get paid on time.

This proactive approach is becoming more common as firms find themselves on stronger financial footing. The 2022 Partner Compensation Survey from Major Lindsey & Africa found that average partner compensation hit $1.12 million—a sign of financial strength that allows for more client-friendly flexibility.

Essential Clauses for Your Attorney Payment Agreement

Your fee agreement has to spell out every detail. Leave nothing to interpretation. Here are the non-negotiable clauses you must include:

- Total Fee and Payment Schedule: State the total amount due. Itemize the exact payment schedule: "An initial deposit of $1,000 is due upon signing, with subsequent payments of $500 due on the 1st of each month for 6 months."

- Automatic Payment Authorization: This is critical. Get explicit, written consent from the client to automatically charge their credit card or bank account on the scheduled dates.

- Default Clause: What happens if a payment is declined? Outline the consequences clearly, including a grace period, a pause in legal work, and your right to withdraw from the case.

Using digital tools like intake form templates can streamline how you gather consent and initial information.

Pro Tip: Don't create a new document. Build this language directly into your standard fee agreement by adding a "Payment Plan Addendum" section.

A solid payment plan process is a core part of scalable law firm operations. If you need a starting point, this legal retainer agreement template provides a foundation you can adapt.

How to Automate Payments and Stop Wasting Time

The biggest fear holding firms back from offering payment plans isn't risk—it's the administrative nightmare of manual tracking and follow-ups. But with the right tools, you can automate the entire process.

Picture this: you send a potential client one secure link. They can review and e-sign your retainer, fill out their intake form, and set up their payment plan. No phone tag. No manual data entry. This is how modern firms operate.

The True Cost of Manual Billing

Managing payments by hand is a direct drain on your firm's profitability. Attorneys already spend 48% of their time on non-billable admin tasks. Chasing invoices and sending reminders fall squarely into that category.

Every minute you or your paralegal spend on manual collections is a minute you aren't spending on billable work. Automation gives that time back to you.

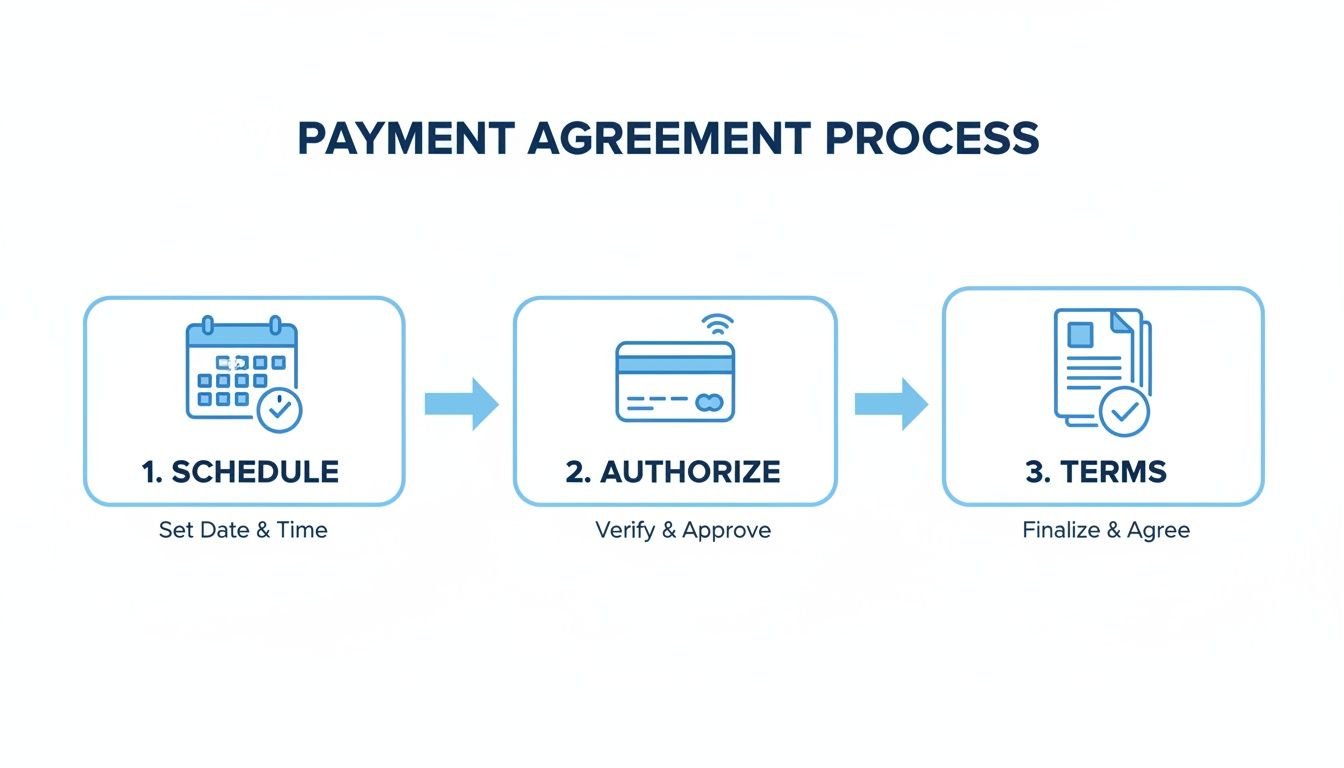

The workflow below shows how simple this can be. Instead of juggling scattered tools and manual follow-ups, a single automated sequence saves you hours per client.

When you consolidate the process for scheduling, authorizing payment, and agreeing to terms, you reduce friction and get retained much faster.

Putting Your Law Firm Payment Plans on Autopilot

Setting up an automated system is simpler than most attorneys think. The goal is a seamless client experience that requires almost no effort from your firm.

Here’s the blueprint:

- Integrate Payments with Intake: Use a platform that bundles e-signatures, intake forms, and payment processing. When a client signs, they are immediately prompted to enter their payment information.

- Authorize Recurring Billing: Your system should securely store the client's payment method (with their consent) and automatically charge it on the agreed-upon schedule.

- Automate Notifications: Let the system handle communication. It should send payment confirmations, reminders, and receipts. If a payment fails, it automatically notifies the client to update their information.

Understanding how lawyers can accept credit cards is a key piece of the puzzle. By automating this workflow, you can confidently offer the payment plans clients want without drowning in administrative work.

Scripts for Discussing Payment Plans with Potential Clients

How you talk about money during a consultation can make or break the deal. Many qualified leads walk away because the fee discussion feels awkward or rigid.

To stop losing these clients, you must get comfortable and confident talking about flexible payment options. This isn't about discounting your services; it's about making your expertise accessible. When you proactively bring up payment plans, you build immediate trust and disarm price objections before they start.

How to Introduce Your Firm's Payment Plans

Stop waiting for potential clients to nervously ask, "uh... do attorneys take payment plans?" Control the conversation. Bringing it up first shows confidence and empathy—two powerful tools for getting hired.

Here are a few simple, effective scripts:

- For Flat-Fee Cases: "Our flat fee for this is $4,000. We typically structure this with an initial $1,000 payment to start, followed by three automatic monthly payments of $1,000. Does that sound manageable?"

- For Retainer-Based Cases: "We start with a $5,000 retainer. To make that easier, we can break it into two payments of $2,500—one now and the second in 30 days. How does that work for you?"

- On Your Website: Add a line to your contact or services page: "We offer flexible payment plans to make quality legal representation accessible. Ask about our options during your consultation."

This proactive approach transforms the fee discussion from a hurdle into a bridge. You’re providing a clear, stress-free path for clients to hire you.

Turning the Conversation into a Conversion

Talking about money this way accelerates their decision to hire you. The data shows leads contacted within five minutes are 21 times more likely to convert. Imagine following a great consultation with one link where they can sign and pay a manageable first installment. You close the gap instantly, getting them retained before they can shop around.

By framing payment plans as a standard part of your process, you make clients feel understood. This small shift is one of the most effective ways to stop losing leads and achieve faster conversions.

Your 4-Step Action Plan to Implement Payment Plans This Week

Enough strategy—let's get this done. You can have automated payment plans running this week by following this clear, four-step process.

Step 1: Finalize Your Payment Models

Decide which structures fit your practice areas. Pick one or two that make sense for your most common cases.

- For Flat-Fee Work: Use a Classic Installment Plan (e.g., a $5,000 fee becomes a $1,000 deposit and four monthly $1,000 payments).

- For Hourly Litigation: Use an Evergreen Retainer that automatically tops up when the balance dips below a set threshold (e.g., $2,000).

Step 2: Update Your Retainer Agreement

Bake clear payment plan language directly into your existing fee agreement. This is non-negotiable for protecting your firm.

Include explicit clauses covering the payment schedule, authorization for automatic payments, and what happens if a client defaults.

Step 3: Connect a Payment Processor

You need a solid system to handle the transactions. Connect a law firm-friendly payment processor like Stripe or LawPay.

These platforms are built to handle payments securely and ethically, which is crucial for staying compliant with trust accounting rules.

Step 4: Automate the Entire Workflow

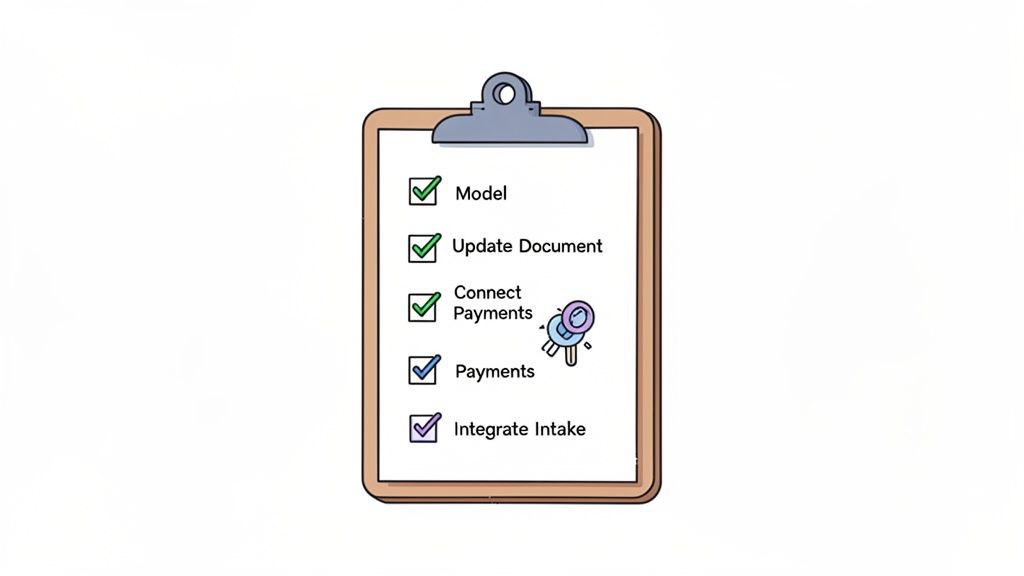

Finally, tie everything together with a unified intake tool. This eliminates the tedious manual work. The goal is to send one link where a client can sign your agreement, fill out their intake form, and set up their payment plan.

This screenshot from intake.link shows how a clean, mobile-friendly interface pulls these steps together. When you integrate signatures and payments into a single flow, you get clients retained on the spot.

FAQs: Your Questions About Attorney Payment Plans Answered

Here are straight answers to the questions we hear most from attorneys.

What Happens If a Client Stops Paying Their Installment Plan?

This is where your retainer agreement earns its keep. It must spell out that you have the right to file a motion to withdraw from the case due to non-payment.

The best defense is a good offense. An automated system flags missed payments immediately, letting you get on top of the situation before it becomes a real problem. A quick call often resolves it.

Are There Any Ethical Rules I Need to Worry About?

Yes, but they boil down to one principle: transparency. The ABA's rules demand that your fee agreement is clear and fair. The total fee must still be reasonable for the work performed.

Always double-check your local bar association's rules on fee agreements and trust accounting to ensure you're fully compliant.

The core ethical requirement is simple: no surprises. The client must understand the total cost, payment schedule, and any late fees before they sign.

Can I Charge Interest or Late Fees on Overdue Payments?

This depends entirely on your state's rules. Many jurisdictions allow reasonable interest or late fees, but this right must be explicitly stated in the signed retainer agreement.

Be specific about the rate and when it kicks in (e.g., a $50 late fee applied if payment is not received within 10 days of the due date). Consult your local ethics rules before implementing any penalty.

Stop losing leads—get signatures before they call another firm.