Stop chasing checks and get paid the moment a client decides to hire you. For a small law firm, the answer to "do attorneys take credit cards?" isn't just yes—it's that you absolutely must, or you're letting revenue slip through your fingers every single day.

Your clients expect to pay with a card. More importantly, your cash flow depends on it.

Why Your Firm Can't Afford to Skip Credit Cards

Waiting for a check to arrive in the mail is an old-school habit that actively costs your firm money and clients. When a potential client has to hunt down a checkbook and a stamp, you're creating friction at the worst possible moment—right when they're ready to commit.

That delay gives a motivated client a window to second-guess their decision or call another firm that makes it easier to get started. According to industry data, 67% of clients choose the first firm that responds professionally. A slow, outdated payment process is the opposite of a professional first impression.

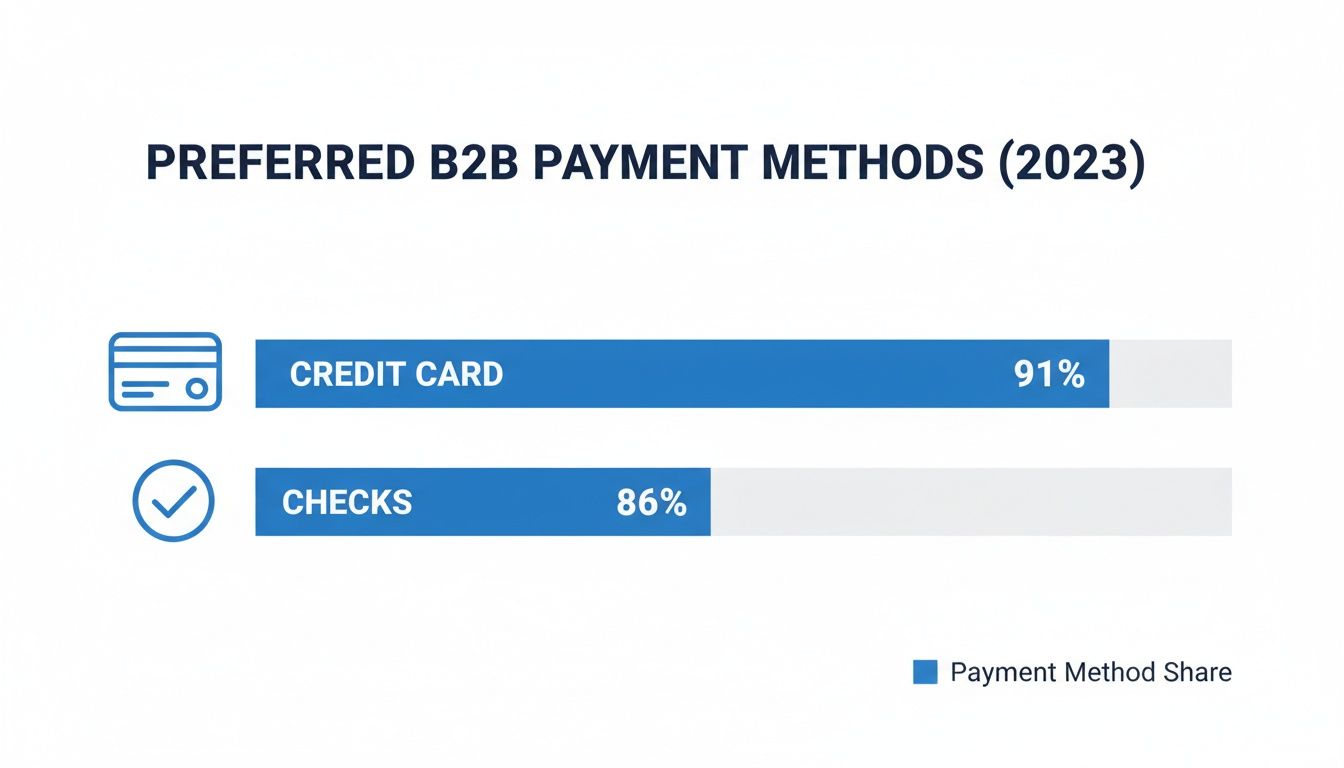

Accepting credit cards is about more than just convenience; it's about speed and conversion. The data clearly shows credit cards have blown past checks as the preferred way to pay, signaling a huge shift in client expectations. Our complete guide to law firm client intake shows how seamless payments are a critical part of winning business.

The numbers don't lie. Offering modern payment options aligns your firm with how people actually manage their money, removing a major barrier to getting hired and paid.

The Financial Impact of Faster Payments

The data proves it: firms that make it easy to pay get paid more, and faster. According to LeanLaw, law firms that accept online credit card payments collect a staggering 33% more revenue than those stuck relying on paper checks.

For a firm billing $2 million, that translates to an extra $54,500 in the bank each year, even after accounting for average processing fees. On top of that, payments arrive four times faster, which can dramatically improve your firm's cash flow.

Credit Cards vs Traditional Checks: A Quick Comparison

This table shows the clear business impact of accepting credit cards versus relying on older payment methods for a small law firm.

| Metric | Accepting Credit Cards | Relying on Checks Only |

|---|---|---|

| Revenue Uplift | +33% higher collection rates | Baseline |

| Payment Speed | 4x faster than checks | Weeks of mail & processing delay |

| Client Experience | Seamless, instant, expected | Cumbersome, slow, outdated |

| Cash Flow | Stable and predictable | Unpredictable, subject to delays |

| Competitive Edge | Aligns with modern client behavior | Creates friction, risks losing clients |

The contrast is stark. This isn't just a small gain; it's a strategic move that directly strengthens your firm's financial stability. Adopting modern payment methods is a key piece of innovation in law that helps small firms win.

How Client Expectations Drive the Need for Card Payments

Let's be direct. Your clients live in a world of one-click checkouts and instant transactions. After they've made the big decision to hire you, asking them to mail a check feels like a major step backward.

That friction is more than an inconvenience; it’s a critical delay. It gives a ready-to-sign client time to second-guess their choice. Or worse, time to call another firm down the street that makes it easy to pay and get started right now. Every hour you wait for a check is an hour a hot lead can go cold.

The Psychology of Payment Friction

The moment a potential client decides to hire you is your point of maximum leverage. Adding hurdles like "mail us a check" immediately breaks that momentum. It feels completely disconnected from how they handle every other important transaction in their lives.

By removing payment friction, you aren't just making things convenient; you are shortening the path from inquiry to paying client. The easier it is for them to pay you, the faster they commit and become your client.

A potential client who has to wait to pay is still just a lead. One who pays the retainer on the spot is a secured client. This is the fundamental difference between a leaky intake process and a modern system built to stop losing leads and close deals faster.

Turning Convenience into a Competitive Advantage

Offering credit card payments is a smart strategic move. Plenty of small firms still cling to old-school methods, creating a clear opportunity for you to stand out. When a client is weighing two similar firms, the one that offers a simple, instant way to pay often wins.

This is especially true in certain practice areas:

- Family Law: Clients are making emotional, time-sensitive decisions. They need a quick and straightforward process, not one that adds more stress.

- Criminal Defense: The need for representation is urgent. The ability to secure a retainer immediately can be the single deciding factor for a client in crisis.

- Business Law: Business owners are busy and accustomed to paying for professional services with corporate credit cards. It’s how they operate.

By making it simple to pay, you send a powerful message from the first interaction: your entire firm is built around efficiency and a modern client experience.

Demystifying Credit Card Processing Fees for Lawyers

Let's get straight to the point about the one thing that makes firm owners hesitate: the fees. Yes, accepting credit cards costs money. But what's the cost of not accepting them?

When you see a processing fee, which usually lands between 1.5% and 3.5%, it's not a single charge. It’s a tiny slice for the card brand (like Visa), another for the payment processor, and one for the bank that issued the card.

How Fees Pay for Themselves

Instead of seeing that fee as a cost, think of it as an investment in getting paid on time.

Imagine a client owes you a $5,000 invoice. A 2.9% processing fee is $145. Now, what’s the alternative? How many non-billable hours will you or your staff spend chasing that check? What’s the risk of that payment arriving 30, 60, or 90 days late—if at all?

Suddenly, trading $145 to get $4,855 in your bank account today sounds like a brilliant business decision. Because it is.

The real cost isn’t the small percentage you pay in fees. It's the administrative hours and lost revenue from an outdated, check-based collections process. This is a foundational part of building smarter law firm operations that don't bog you down.

Navigating the Ethics of Attorney Credit Card Payments

Accepting credit cards is a huge win for your cash flow, but one simple mistake here can land your firm in serious ethical hot water. Remember this: you can never allow processing fees to be deducted from your client trust account (IOLTA).

That money isn't yours yet. Your client's retainer must stay untouched until you’ve earned it. If a standard processor like PayPal deducts a 3% fee from a $5,000 retainer sent to your IOLTA, you've just commingled funds—a major compliance violation.

The IOLTA Compliance Trap

This is where many well-intentioned firms get tripped up. They sign up for a generic payment processor, not realizing the system isn't built to differentiate between your operating and trust accounts.

The core principle is simple: All transaction costs associated with a client's payment must be paid from your firm's operating account, never from client trust funds. Failure to separate these is one of the fastest ways to attract bar scrutiny.

This isn’t a minor bookkeeping error; it’s a fundamental violation of your duty to safeguard client funds. To avoid this landmine, you need a payment system built specifically for legal ethics.

Choosing a Legal-Specific Payment Processor

This is exactly why legal-specific payment solutions were created. They are engineered to solve this precise problem.

When you process a payment through a compliant system, it knows how to handle the money:

- Payment for an Earned Invoice: Funds go to your operating account, and the fee is deducted from that deposit. This is fine.

- Payment for an Unearned Retainer: The full retainer amount goes to your IOLTA account. The processing fee is then billed separately to your linked operating account.

This automated separation guarantees your client trust funds are never touched by fees. Using a processor that understands IOLTA rules isn't a best practice—it's your best defense against accidental ethical violations.

How Law Firms Should Take Credit Card Payments

Ready to stop chasing checks and get paid on time? Smart move. Accepting credit cards isn't complicated, but you need a solid game plan. It starts with picking a payment processor built specifically for the legal industry.

But the best tool isn't just about swiping a card. It's about weaving payments directly into your client intake workflow. Your goal is to kill the awkward dance of sending a retainer, waiting for a signature, and then sending a separate payment link. That gap is where potential clients get cold feet.

Unify Your Intake to Get Paid Instantly

The most effective way for law firms to accept credit cards is to embed the payment step directly into the client intake process. Instead of juggling different tools, a unified system lets you send one link. A new client can click it, sign their retainer, and pay their deposit—all in one seamless motion.

This simple change transforms your intake from a slow, administrative headache into a powerful conversion event. You get a signed agreement and a paid retainer in minutes, not days. You lock in the client before they have a chance to call another firm.

Key Features to Look For

When shopping for a solution, zero in on the features that consolidate your workflow and cut down on manual tasks. Any system you consider must have these three non-negotiables:

- IOLTA-Compliant Processing: The system must automatically route unearned retainers into your trust account and earned fees into your operating account. No exceptions.

- Built-in E-Signatures: Find a tool that lets clients sign their engagement letter and pay from the same screen. Separate links are a recipe for drop-off.

- Practice Management Integration: Your payment and client data should sync directly to your existing software without manual data entry.

This approach is part of building strong accounts receivable best practices that keep your firm financially healthy. And ensuring your payment tool works with your other systems, like a CRM and QuickBooks integration, saves you dozens of admin hours every month.

Expanding Your Payment Options Beyond Credit Cards

Credit cards are just the starting point. To run a truly modern firm, you need a full toolkit of payment methods. Relying only on cards means you’re leaving simpler, cheaper ways to get paid on the table—especially for large initial retainers.

Offering more ways to pay shows your firm is flexible and client-focused. You're removing any friction that might make a potential client pause. It’s a subtle but powerful signal that you’re easy to work with.

Go Beyond Cards with ACH and Payment Plans

While credit cards are king for smaller payments, other electronic options are even better for your bottom line and your client's convenience.

- ACH (eCheck) Payments: Think of these as a direct, digital transfer from your client’s bank account. The killer feature? The processing fees are much lower than credit cards, often capped at a few dollars no matter the payment size. This makes ACH perfect for collecting a hefty retainer where a 3% card fee could cost hundreds.

- Automated Payment Plans: Not every client has cash to pay a large flat fee at once. Offering automated, recurring payment plans makes your services accessible to more people and gives your firm predictable revenue. You can learn more in our guide on whether lawyers accept payment plans.

The legal world’s shift to electronic payments is just catching up to where the rest of society has been for years. You can discover more insights on legal payment trends on Clio's blog. By building a flexible payment system, you’re building robust law firm operations systems that get you paid faster, with less hassle.

Common Questions About Accepting Client Payments

When you're thinking about accepting credit cards at your firm, a few key questions always come up. Here are the straight answers.

Can I Pass Credit Card Fees On to My Clients?

It depends entirely on your state's ethics rules. Some states are fine with passing on processing fees (surcharging) as long as it's transparent. Others flat-out prohibit it.

Before you add a processing fee to a client's invoice, you must check with your state or local bar association. Getting this wrong can lead to serious compliance headaches.

What is the Difference Between LawPay and Stripe?

At first glance, they seem similar, but there's a critical difference. A general processor like Stripe is built for any business and doesn't understand legal trust accounting.

A legal-specific processor like LawPay is designed from the ground up to protect your IOLTA trust account. It ensures processing fees are only ever deducted from your operating account, never from client funds. Standard processors create a massive compliance risk.

Are Credit Card Payments Secure?

Yes, as long as you use a reputable, PCI-compliant payment processor. PCI compliance is the industry security standard that ensures every transaction is encrypted and cardholder data is protected. This protects your firm and gives your clients peace of mind.

Of course, payment security is just one financial question clients have. They often wonder about other costs, like the typical lawyer consultation fee.

With intake.link, you can consolidate your entire client intake process into one simple, secure link. See how intake.link consolidates your entire intake process.