Struggling to sign clients who hesitate at your upfront retainer? Offering a payment plan is the fastest way to turn those "I need to think about it" leads into signed clients. The real question isn't if you should offer payment plans, but how you can automate them to secure more clients without chasing invoices.

Yes, do lawyers take payment plans? The smart ones do. In today's market, potential clients aren't just shopping for the best attorney; they're looking for one they can actually afford. Offering flexible payment options is one of your most powerful conversion tools.

Why Offering a Lawyer Payment Plan Is a Growth Strategy

For a small firm, every lead is precious. Shifting your mindset from "Can I afford to offer this?" to "How do I make this work?" is a crucial step toward scaling your practice. One of the quickest ways to lose a potential client is to create friction around payment. Making your services financially accessible is the single best way to widen your pool of qualified clients and stop losing leads, a key part of our guide to stop losing leads and achieve faster conversions.

This isn't just about being accommodating; it's a direct response to a massive shift in client expectations. Legal costs are climbing, with the average hourly rate for lawyers now at $349. That figure alone puts quality legal help out of reach for a huge segment of the population. As a result, clients are demanding more predictable pricing—a staggering 71% now prefer flat fees over hourly billing. You can discover more insights about lawyer statistics on clio.com.

The Business Case for Payment Flexibility

Adopting payment plans is one of the simplest ways to boost your firm's conversion rate. It removes the single biggest obstacle—a large, intimidating upfront payment—that makes hesitant clients drag their feet or shop around. Remember, leads contacted within 5 minutes are 21x more likely to convert, and payment friction kills that speed.

You’re not just offering a payment schedule; you're providing a clear, manageable path forward. When a potential client sees they can afford your services through manageable installments, their focus shifts from the price tag to the value you provide. This simple change transforms your initial consultation from a price negotiation into a strategy session.

This guide will show you exactly how to implement payment plans without creating a new headache of chasing invoices or putting your cash flow at risk. We'll cover how modern tools can automate the entire process, turning a potential administrative burden into a streamlined system that secures retainers faster.

A quick look at the benefits shows why this isn't just a client-friendly perk—it's a core business strategy.

How Payment Plans Boost Your Firm's Bottom Line

| Benefit | Impact on Your Firm |

|---|---|

| Increased Client Conversion | You sign more of the leads you're already generating by removing the #1 barrier: cost. |

| Wider Client Pool | Your services become accessible to a larger market, not just those who can pay in full upfront. |

| Competitive Advantage | You stand out from firms with rigid payment policies, making your firm the obvious choice. |

| Improved Cash Flow Predictability | Recurring, automated payments create a steady, reliable revenue stream, unlike sporadic lump-sum retainers. |

| Higher Client Satisfaction | Clients appreciate the flexibility, leading to better relationships, positive reviews, and more referrals. |

Offering payment plans fundamentally changes the conversation from "Can I afford this?" to "How do we get started?"—a far more productive place to begin any attorney-client relationship.

Exploring the Smartest Legal Payment Plan Models

So, you’ve decided to offer payment plans. That’s the easy part. The real challenge is picking a model that actually works for your firm without creating a mountain of administrative headaches or confusing your clients.

The right structure makes payments predictable and gets you paid faster. It’s all about moving potential clients from inquiry to retained without the financial friction that kills deals. For a deeper look at how modern firms are thinking about fees, it’s worth reading up on embracing alternative fee arrangements.

Standard Installment Plans

This is the classic, most straightforward approach. It’s a perfect fit for flat-fee services where the scope is well-defined—think uncontested divorces, simple estate plans, or a basic misdemeanor defense. You set the total cost, take a deposit, and schedule the rest in fixed, recurring payments.

For a $6,000 flat-fee case, for instance, you could break it down like this:

- A $2,000 deposit paid upfront to get started.

- Five monthly payments of $800, automatically charged to their card on the 1st of each month.

This gives clients total clarity on what they owe and when. For your firm, it creates a predictable revenue stream.

Evergreen Retainers

For the messy, unpredictable cases—complex litigation, ongoing business counsel—the evergreen retainer is your best friend. It’s designed to end that awkward "we need more money" conversation for good.

Here’s how it works: you and the client agree on a minimum balance to be kept in their trust account, say $2,500. When you bill your time and their balance dips below that floor, your system automatically tops it back up to a pre-agreed amount by charging their card on file. An evergreen retainer transforms your billing from a reactive, manual chore into a proactive, automated workflow.

Hybrid Payment Models

Why choose when you can have the best of both worlds? A hybrid model blends a significant upfront payment with smaller, more manageable installments down the road. This is a fantastic strategy for cases that demand a lot of work at the beginning but will have ongoing costs, like a contested family law matter.

You might ask for a $5,000 upfront retainer to cover discovery and initial filings, then set up $1,000 monthly payments for the next six months to handle the ongoing work. This approach secures a serious commitment from the client from day one while spreading out the remaining cost.

How to Offer Attorney Payment Plans Without Risking Your Cash Flow

Let's be honest. The biggest fear any firm owner has is simple: not getting paid. Offering payment plans can feel like you're just inviting risk, but it doesn’t have to threaten your cash flow. Done right, it becomes a powerful, predictable engine for winning more clients.

Your first line of defense is an ironclad fee agreement. This isn’t just paperwork; it’s a crystal-clear contract that spells out the entire payment schedule, precise due dates, and exactly what happens if a payment is missed. A strong agreement sets expectations from day one and gives you the legal high ground to enforce your terms. You can dive deeper into crafting these essential documents by exploring the fundamentals of a retainer agreement.

Automate Payments to Eliminate Risk

Your second—and most critical—line of defense is automation. The days of chasing checks and sending awkward "your invoice is overdue" emails are over. Instead of leaving payments to chance, modern systems automatically charge the client's credit or debit card on file according to the schedule you both agreed on.

This one shift transforms your revenue from a guessing game into a reliable forecast. It’s no longer a question of if a client will pay, but simply a notification that they have paid. By collecting a solid upfront deposit and automating the rest, you turn a potential financial risk into a secure, predictable revenue stream. You get paid on time, every time, without lifting a finger.

Making Legal Services Accessible and Profitable

This strategy isn't just about protecting your firm; it’s about adapting to the reality your clients face. Recent data shows that as legal fees climb, structured financing is essential for keeping legal services within reach. With partner fees now averaging over $1,100 per hour—an 83% jump in the last decade—many clients simply can't write a massive check upfront.

Offering automated payment plans through integrated platforms is a game-changer, especially for small firms. It bridges the gap, making your services affordable without forcing you to become a collections agency. You can read more about the new boom in law firm financing to understand this market shift.

Here’s how to structure your automated payment plan for maximum security and peace of mind:

- Secure a Strong Deposit: Always collect a meaningful portion of the total fee upfront. This secures the client's commitment and covers your initial work.

- Automate All Future Payments: Use a system that securely stores the client’s payment method and automatically processes scheduled installments. No excuses, no delays.

- Implement a Clear Default Policy: Your fee agreement should state exactly what happens after a failed payment, like a pause in work until the account is brought current.

This automated approach makes the payment process feel seamless and professional from day one. It helps you sign more clients who are ready to hire you but just need a bit of financial flexibility to get started.

The Simple Tech Stack for Automated Client Payments

Let's move from theory to a concrete, modern workflow. Imagine this: you send a potential client a single link. They open it on their phone, see your firm's familiar branding, sign the fee agreement, and enter their card details—all in under five minutes.

That’s it. No follow-up emails, no phone tag, no scanning PDFs. They are officially your client before they even have a chance to call another firm.

Contrast that with the old way. You email a PDF retainer, wait for them to print, sign, and scan it back, then you have to awkwardly ask for credit card numbers over the phone. Every single step is a chance for a lead to go cold. The right technology stack smashes these barriers, cutting down on the non-billable admin work that eats up nearly 48% of an attorney's time.

Building Your Automated Intake Machine

An integrated system isn't a luxury; it's a necessity. You need tools that talk to each other to create a smooth experience for the client and an efficient process on your end. The goal is simple: combine the signature, payment, and intake forms into one unified flow. This approach doesn't just get you retained faster.

For law firms managing diverse payment options, a payment orchestration platform can be a huge asset, unifying different payment gateways and methods under one roof to keep things simple.

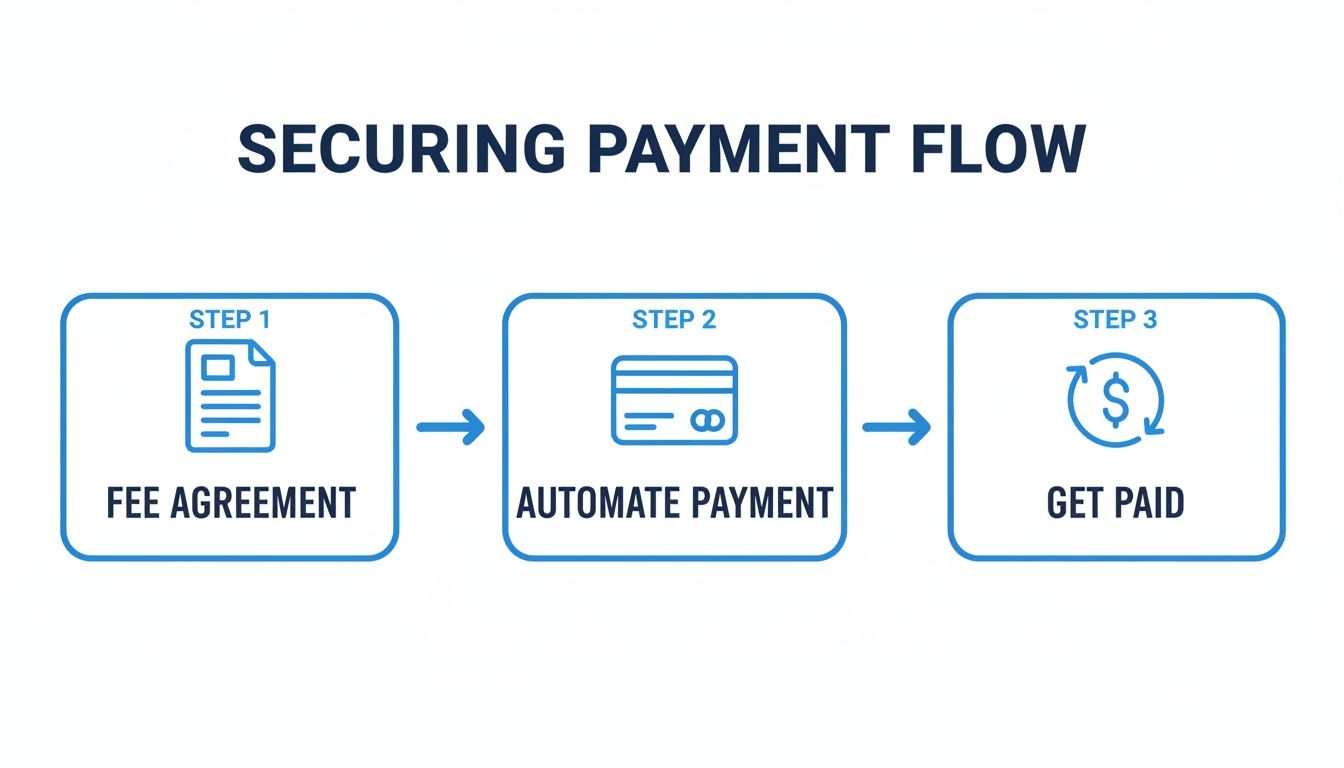

This visual shows the powerful, three-step flow: secure a signed agreement, automate the payment, and get paid without the endless back-and-forth.

This process—agreement, automation, payment—is the engine of a modern firm’s intake system. It turns what was once a multi-day administrative chore into a five-minute conversion.

The Essential Components of Your Stack

Your automated payment stack doesn't need to be complicated. In fact, simpler is almost always better. Here are the core pieces that work together to make it all happen:

- E-Signature Software: This lets clients sign your fee agreement from any device, legally and securely. You want a tool embedded directly into your intake flow, not one that sends clients off to a separate website.

- Online Payment Processor: A compliant processor like Stripe or LawPay is absolutely essential. It needs to handle both one-time deposits and recurring scheduled payments while correctly routing funds to your operating and trust accounts.

- A Central Intake Platform: This is the glue. A platform like intake.link combines the signature and payment steps into a single, branded link you can text or email to a client, creating a completely frictionless journey.

By connecting these tools, you build a system that works for you 24/7. It ensures every new client relationship kicks off with a professional, modern, and incredibly fast experience. For firms aiming to perfect this workflow, choosing the best legal CRM software is a critical step in managing client data from the first click to the final invoice.

Navigating Ethical Rules for Client Payment Plans

Offering payment plans is a great business move, but you have to do it right. Get it wrong, and you risk your license. The absolute foundation of any ethical payment plan is transparency. Your fee agreement isn’t just a contract; it's your primary line of defense for complying with ABA Model Rule 1.5.

You need to spell out everything in that agreement. The total cost, the deposit, the exact payment schedule, due dates, and what happens if a payment is late or missed. Ambiguity is the enemy.

Compliant Fund Management

Beyond the fee agreement, you’ve got to handle the money correctly. This is non-negotiable. Your payment system must be set up to route funds to the right place—either your IOLTA trust account for unearned retainers or your operating account for earned fees. Mess this up, and you’re looking at serious ethical trouble.

Using a generic payment processor like PayPal or Venmo for legal fees is a massive risk. These platforms aren't built for IOLTA compliance and can easily lead to commingling funds, putting your license in jeopardy.

This is especially critical when you consider how burdensome legal costs are for the average person. In the US, liability costs hit 1.66% of GDP—a figure that's a staggering 2.6 times higher than in the Eurozone. That cost pressure makes fee transparency and ethical payment options essential for building client trust. You can learn more about international liability costs from this detailed study.

State-Specific Rule Considerations

Finally, remember the ABA Model Rules are just that—a model. Your state bar has the final say. Before you roll out any payment plan, you absolutely must check your local rules on a few key issues:

- Financing Fees: Can you charge interest or a service fee for the convenience of a payment plan? Some states say yes, others say no.

- Late Payment Penalties: What are the limits on fees you can assess for an overdue payment?

- Handling Defaults: What steps are you allowed to take if a client stops paying? Your response has to align with professional conduct rules.

By getting ahead of these ethical guardrails, you position your firm as both responsible and trustworthy. You turn a smart business decision into a pillar of your professional reputation.

Your Action Plan to Launch Payment Plans Next Week

Feeling ready to stop losing good clients over a single, upfront payment? Good. Let's turn that momentum into a concrete plan you can use to start offering payment plans right away and get retained faster. This isn't some month-long project. You can have this system up and running by next week.

The Five Steps to Launch

Here’s a direct, no-fluff plan to get this done. Each step is designed to be quick so you can see the results almost immediately.

Update Your Fee Agreement: This is your first and most critical step. Add clear, simple language outlining the terms for installment payments. Be sure to include the schedule, the amounts, and your firm’s policy for failed payments.

Choose Your Technology: Don't try to stitch together multiple tools for this. Find a single platform that combines e-signatures and automated, recurring payments into one link. This eliminates the friction that causes great leads to drop off.

Define Your Standard Plans: You don’t need to reinvent the wheel for every client. Create two or three default options for your most common cases (e.g., "$2,000 down and $800 a month for 5 months"). This makes the choice simple for both clients and your team.

Train Your Team: Anyone at your firm who handles intake must be able to explain the payment options confidently and clearly. Honestly, a quick 15-minute meeting is all it takes to get everyone on the same page.

Market Your Advantage: This is a powerful differentiator. Add "Payment Plans Available" to your website's homepage, your email signature, and your social media profiles. Make it impossible for a potential client to miss.

Stop letting your best leads walk away because of sticker shock. By implementing a clear, automated payment plan system, you get retained before a prospect even has a chance to call another firm.

Frequently Asked Questions About Law Firm Payment Plans

These are the direct, no-nonsense answers to the questions we hear most from small firm owners trying to figure out if—and how—to make payment plans work for them.

What Happens If a Client's Scheduled Payment Fails?

This used to be a nightmare, but modern payment systems are built to handle it. A good automated platform will fire off an immediate notification to both you and the client the second a card is declined. Most systems will even re-attempt the charge automatically a few times over the next couple of days.

Your fee agreement is your ultimate safety net. It needs to spell out exactly what happens when a payment fails, including any late fees you’ll charge or if you’ll pause legal work until their account is current. Automation handles that initial, awkward communication, freeing you up to focus on the actual legal work.

Can I Use Payment Plans for Retainers Held in a Trust Account?

Yes, but only if your payment technology is set up correctly. This part is non-negotiable. Payment processors designed specifically for the legal industry are built to direct funds to separate bank accounts.

When you're setting up the system, it's critical to ensure retainer payments are routed directly into your IOLTA or trust account, while any earned fees go straight to your operating account. A platform built for law firms should make this dead simple. Always double-check that your setup aligns with your state bar's trust accounting rules. For a deeper dive, our guide on whether attorneys take credit cards has more details.

Is Using Third-Party Legal Financing a Better Option?

Third-party financing can offload the credit risk, but it often injects a ton of friction right into the middle of your intake process. It forces a potential client—who is ready to hire you—to stop, fill out yet another application, and start a new relationship with a separate company. It’s the perfect moment for them to get frustrated and drop off.

Offering in-house plans through an automated system keeps the experience seamless and entirely under your firm's brand. You maintain full control over the client relationship and eliminate extra steps that cost you conversions. For most small firms, keeping the process simple and fast is the winning play.

Stop losing leads—get signatures before they call another firm.